South African white maize prices may remain high for some time. Here is why and the implications for consumers

The households will have to take some pain in the near term.

| Wandile Sihlobo Jan 4 |

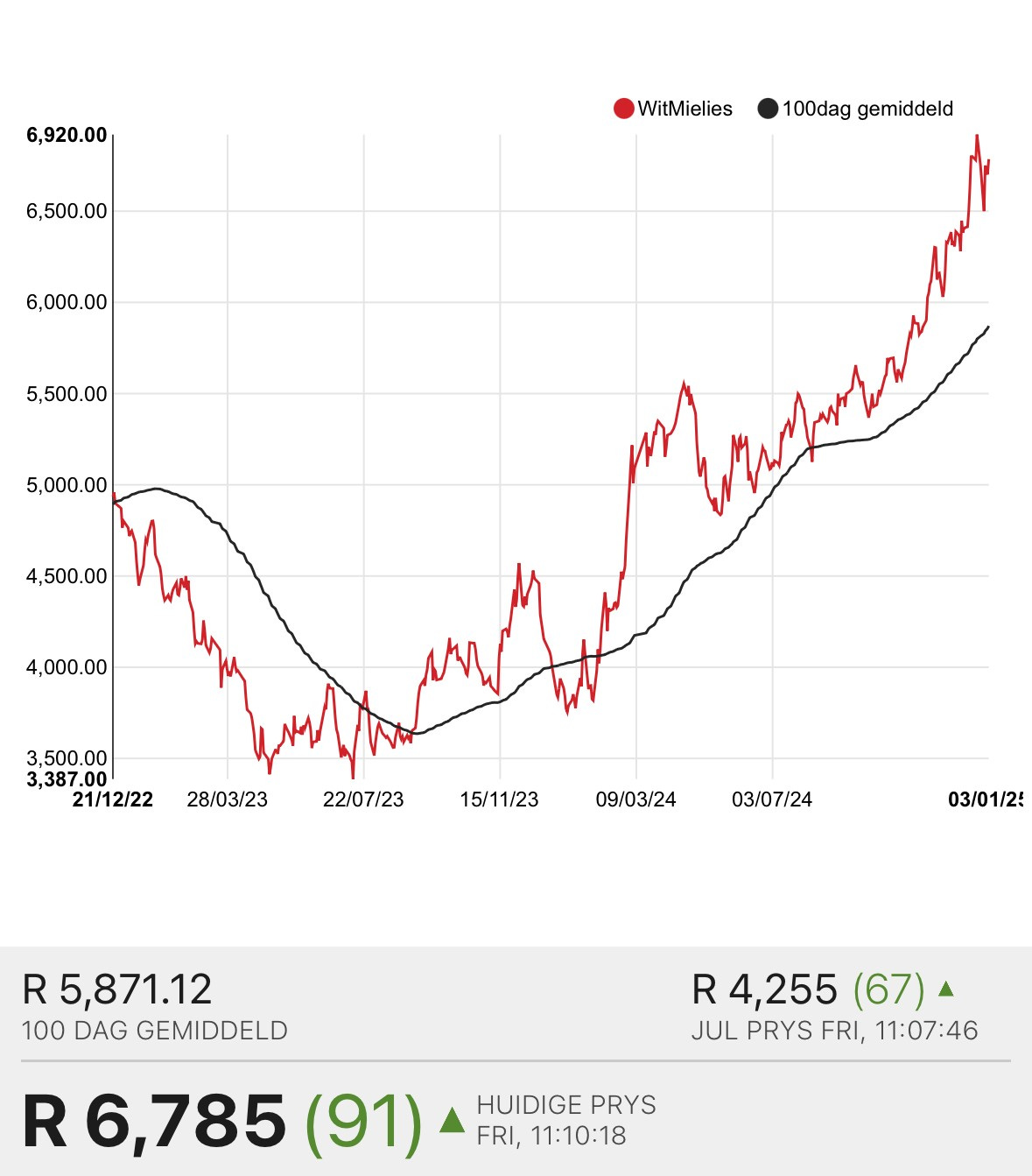

Higher white maize prices in South Africa may be a reality in the first quarter of 2025. Relief may start in the second quarter of the year. On January 3, 2025, South Africa’s white maize spot price traded around R6 871 per tonne, up over 50% from the previous year.

The fundamental challenge we face is that white maize stocks are tight. If we continue using about 428 667 tonnes of white maize monthly, the 2024-25 marketing year may end with closing stocks of just 277 884 tonnes by April 30, 2025.

To understand how tight such closing stocks are, consider the 2023-24 marketing year: the white maize closing stocks were 1.3 million tonnes, and in the 2022-23 marketing year, they were 1.1 million tonnes.

The tighter stocks also imply that South Africa must have early deliveries for the 2025-26 marketing year (which corresponds with the 2024-25 production year) starting May 1, 2025. Such early deliveries would ease some market participants’ concerns about the supplies.

South Africa’s white maize prices (Rand per tonne)

But how did we get here?

The past 2023-24 maize production season (corresponding with the 2024-25 marketing year) was challenging following a mid-summer drought between February and March. The drought resulted in a poor maize harvest across the Southern African region.

Zambia lost half of its maize crop, Zimbabwe lost nearly two-thirds of its maize, and other countries, such as Malawi and Lesotho, also experienced significant maize losses.

South Africa was a slight exception because the impact was less severe than the region. The higher fertilizer usage and improved biotech seed cultivars we use, amongst other things, helped a bit. South Africa’s maize harvest fell by 23% to 12,7 million tonnes. About 6,0 million tonnes is white maize, and 6,7 million tonnes is yellow maize. The overall maize harvest of 12,7 million tonnes is slightly above the annual consumption of 11,7 million tonnes.

The maize harvest (12.7 million tonnes) in the 2023-24 production season, combined with the large carryover stock from the last season (about 2.4 million tonnes), placed South Africa in a relatively comfortable position regarding maize supplies—at least for a moment.

Of the previous season’s 2.4 million tonnes of carryover stock, about 1.3 million tonnes were white maize, and 1.1 million tonnes were yellow maize.

Combining the white maize carryover stock with the white maize harvest for the season meant South Africa had just over 7.0 million tonnes of white maize supplies in the 2024-25 marketing year. With the local white maize demand set to decline to about 5.2 million tonnes, I viewed South Africa as better placed to continue to export to the neighbouring countries. There are few white maize producers in the world. The major producers are South Africa and Mexico. With Mexico facing supply shortages due to unfavourable weather conditions, South Africa was left uniquely responsible for serving the Southern Africa region.

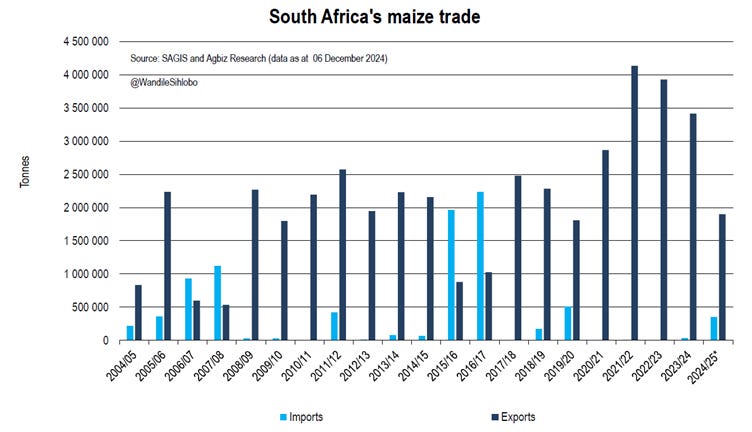

South Africa had sufficient supplies for domestic consumption and exports to the region and continued to export. For example, in the week of December 6, 2024, South Africa exported about 1.4 million tonnes of maize. About 65% of this is white maize, and the remainder is yellow maize. The overall maize export forecast for the season is 1.9 million tonnes (down from 3.4 million tonnes in the 2023-24 marketing year because of the mid-summer drought).

Zimbabwe has been one of the primary beneficiaries, accounting for 55% (788k tonnes) of the 1.4 million tonnes exported in the 2024-25 marketing year. The rest is distributed among Southern African countries, and a small volume is sent to Saudi Arabia.

Moreover, while South Africa will likely remain the net exporter of maize in the 2024-25 marketing year, the coastal regions will import small volumes of yellow maize for animal feed because of price advantage. We have recently seen the imports of yellow maize from Argentina and Brazil through Cape Town. South Africa’s 2024-25 maize imports currently stand at 353k tonnes.

The 2024-25 marketing year started on May 1 2024, and will end by April 2025.

I will update this chart when we get more data and post on X.

What now?

We all knew the 2024-25 market year had heightened uncertainty in the South African maize market. We cannot close the exports. Any policy that suggests such a move would put the Southern African countries that depend on South Africa at immense risk. Such a policy would also reduce South African farmers’ incentive to plant more in the following seasons. Remember – the cure for higher prices is higher prices.

My policy suggestion to government leadership in 2024 was that we must do nothing for the reasons I have explained above and more I wrote here.

I also hoped that the 2024-25 production season (which corresponds with the 2025-26 marketing year) would start early, and we would benefit from the early deliveries. Indeed, farmers were upbeat about the start of the season. South African farmers intend to plant white maize on 1.58 million hectares (up 1% year over year) and yellow maize on 1.06 million hectares (down 2% year over year).

Overall, maize planting intentions are at 2.64 million hectares (up 0.2% year over year), which aligns with the five-year average area. I was at ease, given that we are in the La Niña period, which typically brings above-normal rainfall to Southern Africa.

What changed?

What worries me now is that the rains may have arrived late in some areas and sporadic in some regions. This presents doubt about the size of the early maize producer deliveries. Still, these are anecdotal observations, and we have yet to have a better view of the area planted and the extent of delayed plantings.

However, this uncertainty causes me to believe that white maize prices may be elevated for much of the first quarter (even for a few months until we know the size of the potential harvest) and possibly moderate towards the start of the second quarter when we get the new season harvest.

Another upside risk is the production conditions in Zambia, Zimbabwe, Malawi and other countries in the region. We have yet to have a clearer view of crop conditions, but there are regions to watch closely.

Consumer perspective

From a consumer perspective, grain-related food product prices will rise in the first part of the year. Of course, there will be delays of between three and four months before we see the farm-level prices translate to the retail level. But there should be moderation as the year progresses.

Substitutes such as rice, wheaten products, and potatoes are also available to ease the pressures on households, and these prices have moderated notably in recent months.

Policy recommendation

From a policy perspective, we have limited choices. I remain convinced that we must maintain the current policy path and allow exports.

However, market participants and traders must report trading activity promptly and clearly through SAGIS and other platforms so the market can adjust for grain movements through price. Any other intervention, such as temporarily limiting exports, would have undesirable long-term consequences. I understand the challenge, but South African households will have to deal with some pain in the near term until we get the new season crop in the market.